To open a Business Identification Number (BIN) in Bangladesh, you must register with the National Board of Revenue (NBR). The BIN serves as a unique identifier for businesses and is essential for tax compliance, banking, and participating in tenders.

Step-by-Step Guide to Obtaining a BIN

Prepare Required Documents:

Valid National ID or Passport

Updated Trade License

Taxpayer Identification Number (TIN) certificate

Proof of business address (e.g., utility bill or lease agreement)

Bank account details

Company incorporation certificate (for limited companies)

2. Online Application:

Visit the NBR’s official website.

Create an account or log in.

Fill out the BIN application form with accurate business information.

Upload the required documents.

Submit the application.

3.Receive Your BIN Certificate:

The NBR will review your application.

If approved, you will receive your BIN certificate electronically, usually within a few days.

For a comprehensive guide on BIN registration, including detailed steps and document requirements, you can refer to the Divisional Consultancy’s article: BIN Certificate Total Guide in Bangladesh.

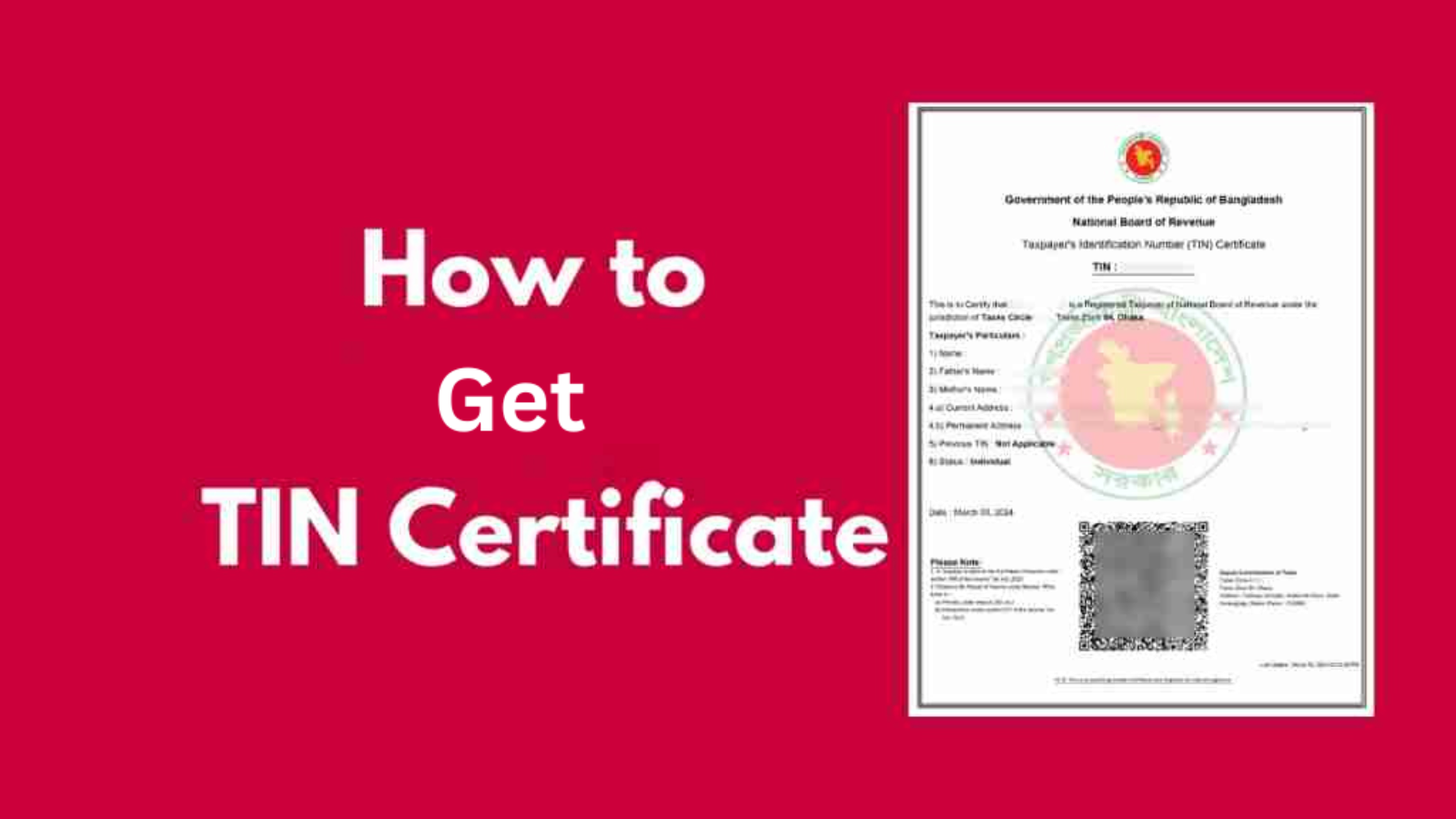

As per the Income Tax Act 2023 of Bangladesh, it is mandatory for all eligible taxpayers—including individuals and companies registered under the Companies Act 1994—to obtain a Taxpayer’s Identification Number (TIN). In today’s digital Bangladesh, getting your e-TIN certificate is simple, fast, and entirely free.

Whether you’re an entrepreneur, a salaried individual, or a business owner, having a TIN certificate is essential for various financial and legal processes like opening a bank account, applying for loans, or filing income tax returns.

What is a TIN Certificate?

TIN stands for Tax Identification Number or Taxpayer’s Identification Number. It is a 12-digit unique number issued by the National Board of Revenue (NBR) of Bangladesh. When you obtain it digitally, it’s referred to as an e-TIN.

Why Do You Need a TIN Certificate?

Legal Obligation under the Income Tax Act 2023

Required for filing income tax returns

Mandatory for company registration and business operations

Required for bank loan applications and trade licenses

Helps in ensuring tax compliance

Two Ways to Get a TIN Certificate

You can register for a TIN certificate using two methods:

1. Online Process (e-TIN Registration)

The online registration is fast, free, and can be completed in under 10 minutes if you have all the necessary information ready.

Provide your name, NID number, mobile number (active Bangladeshi number), and complete the captcha.

The email field is optional.

Receive the Activation Code:

You will receive a 5-digit activation code via SMS.

Activate Your Account:

Enter the code on the activation page and click ‘Activate’.

Login to Your Account:

Use the generated User ID and Password to log in.

Start Registration:

Click on “(For TIN Registration/Re-registration Click here).”

Choose your taxpayer status: Individual (default) or Company.

Enter Basic Information:

Enter your full name, address, date of birth, NID/passport info, etc.

Review Your Application:

Check all the details in the final preview.

Submit Application:

If everything is correct, click ‘Submit Application’.

Get Your Certificate:

Your e-TIN certificate will be generated immediately.

Options: View, Print, Save, or Email your certificate (PDF format).

✨ Pro Tip: Always save a digital copy of your certificate for future use to avoid system issues or website downtime.

2. Manual Process (Offline Registration)

You can also register manually by visiting the nearest NBR office. This method involves:

Submitting a photocopy of your NID

Passport-sized photographs

Personal and/or business details

An officer at the NBR office will manually input your data into the system. The process may take 2-3 working days. However, this method is not recommended due to:

Travel costs

Time-consuming procedures

Potential unexpected expenses

❌ Manual method is less efficient and not encouraged unless absolutely necessary.

With Bangladesh’s tax system now digitalized, getting your e-TIN certificate has never been easier. It saves you time, money, and unnecessary hassle. Just follow the simple online process, and you can secure your e-TIN certificate in minutes.

So, why wait? Visit secure.incometax.gov.bd today and complete your e-TIN registration hassle-free!

For any professional assistance regarding tax registration or compliance services, feel free to consult a licensed Chartered Secretary, Tax Practitioner, or Legal Advisor.

The corporate tax landscape in Bangladesh as of 2025:

Corporate Income Tax Rates

Publicly Traded Companies: Subject to a tax rate of either 22.5% or 25%, depending on specific conditions and exceptions.

Non-Publicly Traded Companies: Generally taxed at 27.5%, with certain exceptions applicable.

Standard Rate Adjustment: The standard corporate tax rate was reduced from 27.5% to 25%, effective from 1 July 2024.

Minimum Tax Regime

Companies are required to compute their tax liability using three methods and pay the highest amount:

Regular Tax on Profits: Based on net income.

Withholding Tax (WHT): Applicable under certain sections.

Tax on Gross Receipts: Applicable to companies with gross receipts over BDT 5 million and other persons with gross receipts over BDT 30 million.

Taxation Scope

Resident Companies: Taxed on their global income.

Non-Resident Companies: Taxed only on income that is received in Bangladesh or that accrues or arises in Bangladesh.

Tax Filing Deadlines

Companies must file their income tax returns by the 15th day of the seventh month following the end of the income year. However, if this date falls before 15 September, the due date is extended to 15 September.

Additional Notes

Tax on Non-Filers: A 20% tax is levied on the gross income of companies not obligated to file a return, with certain exemptions.

Historical Context: The corporate tax rate in Bangladesh has averaged 29.82% from 1997 to 2024, peaking at 40.00% in 1998 and reaching a low of 25.00% in 2016.

In Bangladesh, the government offers tax holiday incentives to encourage investment in various industrial sectors, aiming to promote economic growth and regional development. These incentives vary based on the location of the industry and the specific sector involved.

Duration and Scope of Tax Holidays:

General Industries: Industries established in developed regions, such as Dhaka and Chittagong (excluding certain hill tracts), are eligible for a tax holiday of 5 years. The tax exemption schedule typically starts with a 100% exemption in the first year, followed by 50% in the subsequent two years, and 25% in the fifth year.

Less Developed Regions: Industries set up in less developed areas receive a tax holiday of 7 years, with a structured exemption rate starting at 100% in the first three years, 50% in the next three years, and 25% in the seventh year.

Least Developed Regions and Export Processing Zones (EPZs): Industries located in the least developed areas and EPZs can enjoy tax holidays for 9 to 12 years, with full exemptions in the initial years, gradually decreasing over the tenure.

Recent Developments:

In an effort to enhance industrialization and export earnings, the Bangladesh Economic Zones Authority (BEZA) has approved the establishment of 29 private economic zones, with eight already operational. Investors in these zones are granted a 10-year tax holiday, which includes a full tax waiver in the first three years, followed by 80%, 70%, and 60% exemptions in the subsequent years.

Expansion of Eligible Sectors:

The government has extended tax holiday benefits to additional sectors to diversify industrial growth. Recent amendments include seven new sectors alongside the existing 26, aiming to attract investment in areas such as manmade fiber production and motorcycle manufacturing. These sectors are now eligible for tax holidays ranging from 5 to 10 years, depending on their location and compliance with specified criteria.

Special Considerations:

The government has also extended tax holiday facilities to private power generation companies. Companies that commence commercial production by June 30, 2024, are exempt from income tax for the first five years, with reduced rates in the subsequent years. Additionally, these companies benefit from exemptions on royalties, technical fees, and capital gains taxes.

Policy Discussions and Reforms:

There is an ongoing dialogue regarding the effectiveness and impact of tax holiday policies. Discussions focus on ensuring that these incentives align with national development goals, promote equitable regional growth, and attract investments in high-priority sectors. Recommendations include revisiting the policy to extend support to emerging sectors and conducting comprehensive analyses of the economic benefits of tax holidays.

These tax holiday initiatives are part of Bangladesh’s broader strategy to stimulate industrialization, create employment opportunities, and enhance export revenues, thereby contributing to the nation’s economic development.

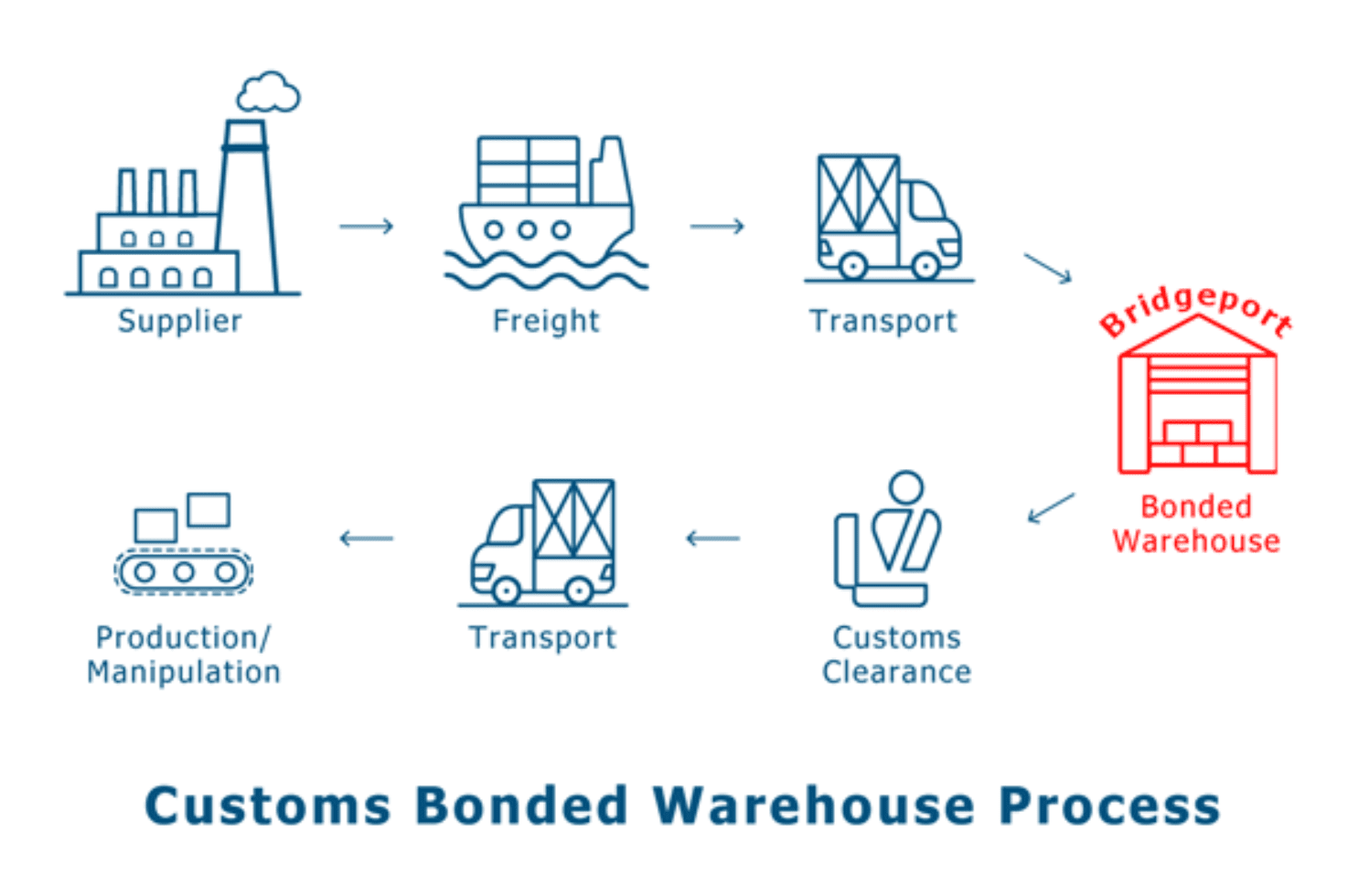

In Bangladesh, bonded warehouses are facilities authorized by the National Board of Revenue (NBR) that allow export-oriented industries to import raw materials and packaging materials without immediate payment of customs duties and taxes. This system aims to enhance the competitiveness of Bangladeshi exports by reducing production costs and streamlining the import process.

Categories of Bonded Warehouses:

Special Bonded Warehouses (SBW): These are designated for 100% export-oriented ready-made garment (RMG) industries, including woven garments, knitwear, and sweater manufacturing.

General Bonded Warehouses (GBW): These apply to other 100% export-oriented industries, such as shipbuilding, accessories manufacturing (e.g., packing materials, labels, buttons), and certain home consumption industries (e.g., sugar, vegetable oil, leather, tobacco).

Benefits of Bonded Warehousing:

Duty-Free Imports: Industries can import necessary materials without paying customs duties upfront, improving cash flow and reducing production costs.

Deferred Duty Payment: Duties are paid only when goods are cleared from the warehouse for domestic sale, allowing businesses to manage working capital more effectively.

Storage Flexibility: Imported goods can be stored for extended periods (up to two years for export-oriented industries), providing flexibility in inventory management and production planning

Facilitated Export Processes: Bonded warehouses streamline the export process by allowing direct export of goods without the need for customs clearance at the port, saving time and reducing logistical complexities.

To utilize bonded warehousing facilities, businesses must obtain a bond license from the Customs Bond Commissioner ate. The application process includes submitting various documents, such as business registration, tax identification number, trade license, and financial statements, among others.

custom-bonded-warehouse-process

It’s important to note that while bonded warehouses offer significant advantages for export-oriented industries, regulations and procedures are subject to change. Therefore, businesses should regularly consult official sources or seek professional advice to ensure compliance with current laws and regulations.