In Bangladesh, VAT Deduction at Source (VDS) is a mechanism where certain designated entities are required to deduct Value Added Tax (VAT) from payments made to suppliers or service providers at the time of payment. This system ensures the collection of VAT at the source, facilitating compliance and revenue collection.

Who Must Deduct VAT at Source?

The following entities are mandated to withhold VAT under the VDS system:

Government entities

Non-governmental organizations (NGOs) approved by the NGO Affairs Bureau or the Directorate General of Social Welfare

Banks, insurance companies, and similar financial institutions

Secondary or post-secondary educational institutions

Limited companies

Entities with an annual turnover exceeding BDT 100 million

When Is VDS Applicable?

VDS is applied when these entities procure specific goods or services. For instance, services such as those provided by air-conditioned hotels are subject to a 15% VDS rate, while non-air-conditioned hotels are subject to a 7.5% rate.

Key Points to Note

VDS is not an additional tax but a method of collecting VAT at the source.

The responsibility to deduct and remit VAT lies with the withholding entity.

Proper documentation, such as VAT invoices and certificates, is essential to ensure compliance.

This system is designed to streamline VAT collection and reduce evasion by capturing tax at the point of transaction.

Withholding tax (WHT) refers to the income tax that a payer (either resident or non-resident) is obligated to deduct at the source when making certain specified payments. This mechanism ensures tax collection at the point of payment, streamlining the process for both the payer and the government.

Key Aspects of Withholding Tax in Bangladesh

Obligation to Withhold: Payers are required to withhold tax when making payments such as salaries, execution of contracts, supply of goods, manufacturing, printing, royalties, services, commissions, rent, dividends, and payments to non-residents. NBR Bangladesh

Withholder Identification Number: Every person responsible for deducting or collecting tax must obtain a Withholder Identification Number. Worldwide Tax Summaries Online

Filing Returns: Entities must file a Return of Withholding Taxes under Section 75A of the Income Tax Ordinance, 1984. The first return is due by January 31 of the financial year in which the deduction or collection was made, and the second return by July 31 of the following financial year.

Schedules and Documentation: Specific schedules (e.g., 24AA, 24AB, 24AC) must be attached to the return, detailing the sources and amounts of tax withheld.

This system ensures that the government receives tax revenues promptly and reduces the burden on taxpayers by collecting taxes at the source of income.

To open a Business Identification Number (BIN) in Bangladesh, you must register with the National Board of Revenue (NBR). The BIN serves as a unique identifier for businesses and is essential for tax compliance, banking, and participating in tenders.

Step-by-Step Guide to Obtaining a BIN

Prepare Required Documents:

Valid National ID or Passport

Updated Trade License

Taxpayer Identification Number (TIN) certificate

Proof of business address (e.g., utility bill or lease agreement)

Bank account details

Company incorporation certificate (for limited companies)

2. Online Application:

Visit the NBR’s official website.

Create an account or log in.

Fill out the BIN application form with accurate business information.

Upload the required documents.

Submit the application.

3.Receive Your BIN Certificate:

The NBR will review your application.

If approved, you will receive your BIN certificate electronically, usually within a few days.

For a comprehensive guide on BIN registration, including detailed steps and document requirements, you can refer to the Divisional Consultancy’s article: BIN Certificate Total Guide in Bangladesh.

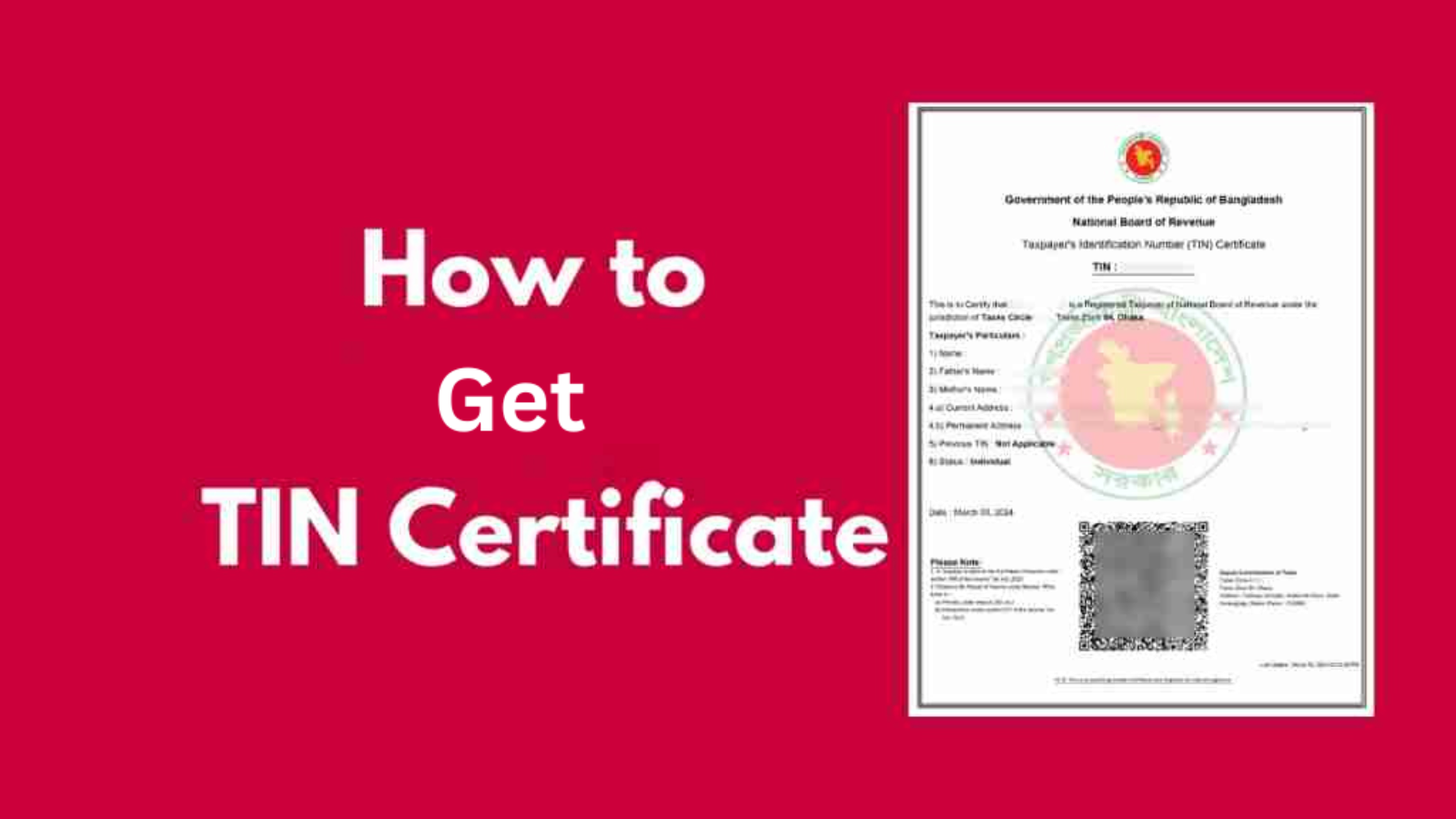

As per the Income Tax Act 2023 of Bangladesh, it is mandatory for all eligible taxpayers—including individuals and companies registered under the Companies Act 1994—to obtain a Taxpayer’s Identification Number (TIN). In today’s digital Bangladesh, getting your e-TIN certificate is simple, fast, and entirely free.

Whether you’re an entrepreneur, a salaried individual, or a business owner, having a TIN certificate is essential for various financial and legal processes like opening a bank account, applying for loans, or filing income tax returns.

What is a TIN Certificate?

TIN stands for Tax Identification Number or Taxpayer’s Identification Number. It is a 12-digit unique number issued by the National Board of Revenue (NBR) of Bangladesh. When you obtain it digitally, it’s referred to as an e-TIN.

Why Do You Need a TIN Certificate?

Legal Obligation under the Income Tax Act 2023

Required for filing income tax returns

Mandatory for company registration and business operations

Required for bank loan applications and trade licenses

Helps in ensuring tax compliance

Two Ways to Get a TIN Certificate

You can register for a TIN certificate using two methods:

1. Online Process (e-TIN Registration)

The online registration is fast, free, and can be completed in under 10 minutes if you have all the necessary information ready.

Provide your name, NID number, mobile number (active Bangladeshi number), and complete the captcha.

The email field is optional.

Receive the Activation Code:

You will receive a 5-digit activation code via SMS.

Activate Your Account:

Enter the code on the activation page and click ‘Activate’.

Login to Your Account:

Use the generated User ID and Password to log in.

Start Registration:

Click on “(For TIN Registration/Re-registration Click here).”

Choose your taxpayer status: Individual (default) or Company.

Enter Basic Information:

Enter your full name, address, date of birth, NID/passport info, etc.

Review Your Application:

Check all the details in the final preview.

Submit Application:

If everything is correct, click ‘Submit Application’.

Get Your Certificate:

Your e-TIN certificate will be generated immediately.

Options: View, Print, Save, or Email your certificate (PDF format).

✨ Pro Tip: Always save a digital copy of your certificate for future use to avoid system issues or website downtime.

2. Manual Process (Offline Registration)

You can also register manually by visiting the nearest NBR office. This method involves:

Submitting a photocopy of your NID

Passport-sized photographs

Personal and/or business details

An officer at the NBR office will manually input your data into the system. The process may take 2-3 working days. However, this method is not recommended due to:

Travel costs

Time-consuming procedures

Potential unexpected expenses

❌ Manual method is less efficient and not encouraged unless absolutely necessary.

With Bangladesh’s tax system now digitalized, getting your e-TIN certificate has never been easier. It saves you time, money, and unnecessary hassle. Just follow the simple online process, and you can secure your e-TIN certificate in minutes.

So, why wait? Visit secure.incometax.gov.bd today and complete your e-TIN registration hassle-free!

For any professional assistance regarding tax registration or compliance services, feel free to consult a licensed Chartered Secretary, Tax Practitioner, or Legal Advisor.

The corporate tax landscape in Bangladesh as of 2025:

Corporate Income Tax Rates

Publicly Traded Companies: Subject to a tax rate of either 22.5% or 25%, depending on specific conditions and exceptions.

Non-Publicly Traded Companies: Generally taxed at 27.5%, with certain exceptions applicable.

Standard Rate Adjustment: The standard corporate tax rate was reduced from 27.5% to 25%, effective from 1 July 2024.

Minimum Tax Regime

Companies are required to compute their tax liability using three methods and pay the highest amount:

Regular Tax on Profits: Based on net income.

Withholding Tax (WHT): Applicable under certain sections.

Tax on Gross Receipts: Applicable to companies with gross receipts over BDT 5 million and other persons with gross receipts over BDT 30 million.

Taxation Scope

Resident Companies: Taxed on their global income.

Non-Resident Companies: Taxed only on income that is received in Bangladesh or that accrues or arises in Bangladesh.

Tax Filing Deadlines

Companies must file their income tax returns by the 15th day of the seventh month following the end of the income year. However, if this date falls before 15 September, the due date is extended to 15 September.

Additional Notes

Tax on Non-Filers: A 20% tax is levied on the gross income of companies not obligated to file a return, with certain exemptions.

Historical Context: The corporate tax rate in Bangladesh has averaged 29.82% from 1997 to 2024, peaking at 40.00% in 1998 and reaching a low of 25.00% in 2016.